The Great Public Pension Plan Tsunami — It’s Coming! (It’s Already Here!)

Public employees have challenged the reduction or elimination of pension COLAs in states such as Colorado, Minnesota, and S. Dakota. Courts in the first two states said that the changes were not unconstitutional per se but also indicated that changes to the base pension formula likely were off limits for current employees. Previously, courts in California and W. Virginia had said COLA cuts were unconstitutional. The reduction of COLAs would provide immediate cash savings to states unlike formula reductions limited to only future hires.

However, in August 2016 a significant decision by the California appellate court in San Francisco that upheld the trial court’s decision against the Marin Association of Public Employees that the legislature’s new pension calculations affecting current employees didn’t violate workers’ vested rights. It also said that lawmakers have the power to change the formula before retirement: “While a public employee does have a ’vested right’ to a pension, that right is only to a ’reasonable’ pension– not an immutable entitlement to the most optimal formula of calculating the pension.” The court didn’t define what’s reasonable which will lead to more litigation. The case is sure to be appealed to the State Supreme Court.

Lawsuits are pending in other states (e.g., FL, NH) as workers challenge increased paycheck deductions and contributions toward their pensions.

http://www.nytimes.com/2011/07/01/business/01pension.html?_r=2&nl=todaysheadlines&emc=tha25

For additional updates: http://www.statebudgetsolutions.org/publications/detail/state-pension-litigation-update-november-2012 ; http://www.governing.com/finance101/gov-pension-protections-state-by-state.html

https://www.nasra.org/files/Spotlight/Significant%20Reforms.pdf

We like this passage from The Hill (4/11/12): “The thing that pushes the United States over the tipping point just might be the exploding state pension crisis…. It is clear that many states are now teetering on the brink of bankruptcy as a result of pension promises made to employees, the enormous bill for which is just beginning to come due…. [B]ankrupt states with huge pension obligations will look to the federal government to make up the difference. Are we prepared to offer a rescue to these states that will make the bailouts of the last few years look insignificant by comparison?”

____________________________________

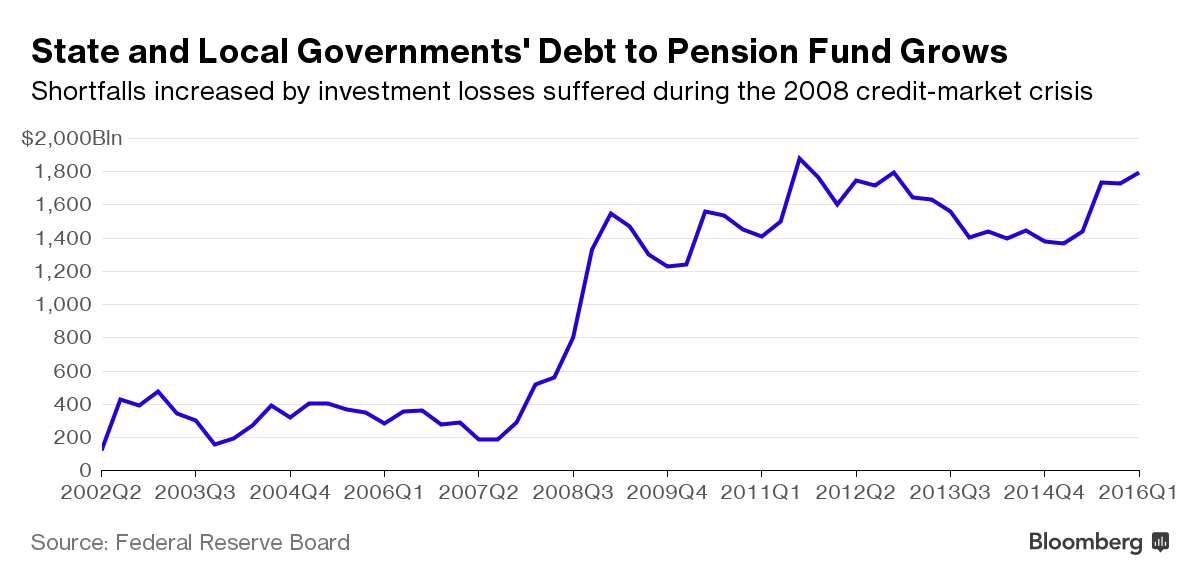

“The ability of local governments, particularly cities, to provide the levels of service they do now is threatened by this liability,” said Joshua Rauh, a Northwestern University professor and co-author with Robert Novy-Marx, a University of Rochester professor, of a report released October 12, 2010. The report says that five major cities — Boston, Chicago, Cincinnati, Jacksonville and St. Paul — have pension assets that can pay for promised benefits only through 2020, and Philadelphia has assets on hand that can only pay pension promises through 2015. Rauh says that local governments should trim benefits by raising retirement ages for participants and lowering COLAs, then refinance pension debt and spread it out into the future. New employees should be shifted to defined-contribution plans.

________________________________________

The NY Times reported on April 25, 2011 how some states, like Michigan, have given plenary power to fiscal managers to deal with financially strapped cities and towns. Similarly, an arbitrator recently decided that Detroit could not freeze its pension fund immediately but agreed that the city could reduce the rate at which certain police officers earn pension future benefits from 2.5% of pay to 2.1%. While such a reduction for current workers is rare, the small change will not really solve Detroit’s pension problems where there are twice as many retirees as those working.

The story also notes that Prichard, AL, a small city near Mobile, the pension fund ran out of cash in 2009 and the city stopped sending pension checks to its 150 retired workers. The article is here: http://www.nytimes.com/2011/04/26/us/26pensions.html

________________________________________

The NY Times reported in early December 2010 that rising concern over local government finances may require that they provide better disclosures if they want to issue new bonds. Such disclosures are likely to lead to pressure from bond underwriters to rein in pension costs which in turn will be resisted by public employee unions and their considerable political clout, placing politicians in a very hot seat indeed.

________________________________________

In a related development, the SEC has challenged at least two states on the lack of adequate disclosure in their bond financing documents of potential risks from pension underfunding. No penalties so far, just a requirement of more disclosure to current and future bondholders.

________________________________________

The NY Times reported on 1/18/2011 that Moody’s now will add states’ unfunded pension obligations together with the value of their bonds, and consider this total liability when rating their credit. The new approach will be more comparable to how it rates corporate debt and sovereign debt. Moody’s did not indicate whether states’ credit ratings may rise or fall but it can’t be good.

________________________________________

The Public Employee Pension Transparency Act, H.R. 6484, backed by key House Republicans would bar the federal government from bailing out public plans and deny federal tax exemption for bonds issued by governmental entities that don’t comply with the new disclosure requirements. The enhanced disclosures would require use of new actuarial assumptions that could dramatically expand the size of pension liabilities. Rep. Devin Nunes, R-Calif., who introduced the bill on Dec. 2, said “If we ignore these warnings, we will have learned nothing from the subprime mortgage crisis.” Representatives of state and local governments and unions counter that the bill is a federal assault on state and local government autonomy and an attack on defined benefit plans.

________________________________________

Newt Gingrich and Grover Norquist (that’s a tongue twister) are pushing for legislation that will allow state governments to file for bankruptcy under Chapter 9 to cut pension benefits that they can’t otherwise reduce. Local municipalities already have access to Chapter 9. Of course, public pensions are not backed by a PBGC guaranteed minimum benefit in the event of bankruptcy. No Congressional sponsor has yet been found for this proposal.

________________________________________

A recent study by the National Center for Policy Analysis analyzed 153 state and local pension plans, representing more than 85 percent of such total pension liabilities, and recalculated these liabilities using a lower (i.e., more reasonable) discount rate. A discount rate is used to determine the current value of the plan’s future benefit obligations. A higher discount rate will reduce the size of a pension plan’s accrued liabilities. The Center’s recalculations: unfunded pension liabilities are approximately $2.5 trillion, over 5x greater compared to the current reported amount of only $493 billion! The full report is at http://www.ncpa.org/pdfs/st329.pdf.

________________________________________

State elected officials have long treated pension reform as a political “third rail” due to the influence of public unions, self-interest and other factors. However, seven states, including Arizona, Illinois and New Jersey, have reformed their pension systems this year, and others are pushing for similar changes. Illinois’ reforms, enacted at the end of March, have garnered attention and drawn anger from unions. The state raised the retirement age to 67 from 55, and reduced the maximum allowed pension. However, these reforms only apply to workers entering the work force in 2011 (doesn’t sound that bad to us). This prospective fix is generally the reform pattern being followed because state law consistently defines a public pension as a contract between the state and its employees that cannot be impaired.

> Nine states protect public employees in their constitutions: Alaska, Arizona, Hawaii, Illinois, Louisiana, Michigan, New Mexico, New York and Texas.

In states without constitutional guarantees, many statutes and court cases nonetheless consider public retirement benefits an unbreakable contract. That same protection arguably is in the contract clause of the U.S. Constitution, which says: “No state shall … pass any … law impairing the obligations of contracts.”

While most state plans have primarily focused on cutting benefits for new hires, another common tactic to save money is to decrease the COLA formula. This is permissible because the plans are not subject to ERISA. However, some State courts have determined that COLA increases, which keep pension income on pace with inflation, are part of a worker’s benefits that cannot be diminished. Nonetheless, Colorado (67% funded), Minnesota (70% funded) and South Dakota (92% funded) lawmakers have limited COLAs for existing retirees and workers and are hoping that the courts will agree that the financial turmoil for public pension systems calls for a new approach because there is no other realistic alternative. The same law firm (Stember Feinstein) is representing the participants in all three lawsuits challenging these changes.

The states likely will argue that these COLA changes are a minor modification to the pension contract that is reasonable and necessary to avoid the more important public purpose of avoiding fiscal default. For example, in Ohio, the unions and the State have negotiated a reduction in the COLA formula.

________________________________________

A NY Times story on July 21, 2010 described another aspect of this perilous pension situation involving approximate six million public employees who still work outside the Social Security system: teachers in California, Illinois and Texas, and nearly all state workers in Alaska, Colorado, Massachusetts, Nevada, Ohio, Louisiana, and Maine.

Why are these workers outside Social Security when all other states and the federal government now participate in it? Basically, these states are the remaining holdouts who thought they could provide richer pensions at a lower cost, both to workers and taxpayers. However, to provide richer benefits with smaller contributions (both employee and employer) than the combined payroll tax for Social Security is proving increasingly difficult. This is particularly so with generous plan designs that permit full retirement 10 or more years earlier than Social Security retirement age, questionable overtime practices that allow padding of the plans’ final average pay formulas, dubious temporary promotions providing entitlement to higher pension calculations (sometimes seen with firefighter and police plans), and relaxed disability standards that permit retirement at at even earlier ages with tax-free benefits under state law.

One thing still helping these plans is that many government employees leave before becoming fully vested or earning a significant benefit under the typical plan formula. For example, in Maine only one in five state employees stays around long enough to get a full pension. The majority leave, taking neither a pension nor any Social Security credits. This practice, not investment performance, has sustained many state pension systems to date.

The other reason state pension plans thought they could beat Social Security was investment return. This strategy looked good during the 1982-2000 market boom but not so after the 2001-2009 “lost” investment decade. Moreover, the plan investment return assumptions (and discount factors) were often overstated, in large part due to political concerns to keep contributions (i.e., taxes) lower.

Some state pension plans now have shortfalls so large that they need huge contributions — now. Almost all state pension funds have had big losses of late, but these “go-it-alone” states appear to be in even worse shape.

Defenders of public employee pensions – which are generally 3x-4.5x better than the Social Security benefit – used to claim that there was little cost to the public for this disparity because (1) the generous benefit offsets decreased career pay vs. comparable private sector jobs, and (2) much of the funds necessary to pay benefits come from investment return, and not the burden of the taxpayer. This no longer appears to be the case.

So how does switching to Social Security help the state and its plan? Gradually at best. Depending on state law and the plan, the change only may be allowable for future hires who would receive Social Security and a reduced benefit under the pension plan. This reduced future liability can help to gradually reduce the amount of contributions in excess of the added Social Security cost. Another approach is to move all current employees into Social Security on either a mandatory or elective basis with a corresponding decrease in future pension accruals. Interestingly, a state worker (e.g., age 55) who will retire with less than the required 10 years of Social Security service may not receive a benefit for the period paid in.

Other options to pension reforms to save money? We can expect states to try to increase the cost to retirees of their health benefits. However, if this is permissible, we don’t see why employees can’t be asked to contribute more to their pensions. Is the difference that the retiree is no longer an employee and/or the contract right to health benefits is not the same as to a specific pension benefit?

_____________________________________________________

On June 9, 2016 the New Jersey Supreme Court ruled that retired public employees do not have a contractual right to receive increasing COLAs, a decision that is expected to save the state billions of dollars. Credit rating agencies rank NJ the second-worst U.S. state, behind only Illinois, in part because of its growing pension costs and narrow reserves. [Berg v. Christie, No. 074612] [CNBC also noted: In 2011, New Jersey legislation froze COLAs at the 2011 level for current and future qualifying retirees.